The Ugly Truth: The Ugly Math of Venture Capital: Why "Nobility" is a Poor Operating System

Prashant Rao

Venture capital is sold as visionary investing: brilliant partners spotting the future, backing disruptive teams, and reaping massive rewards through pattern recognition and conviction.

The media loves the narrative—hoodies at Davos, unicorn origin stories, “genius” bets on the next big thing.

But let’s strip away all the glamour, the prestige, the marketing, and look at early-stage VC purely as a mathematical and scientific problem.

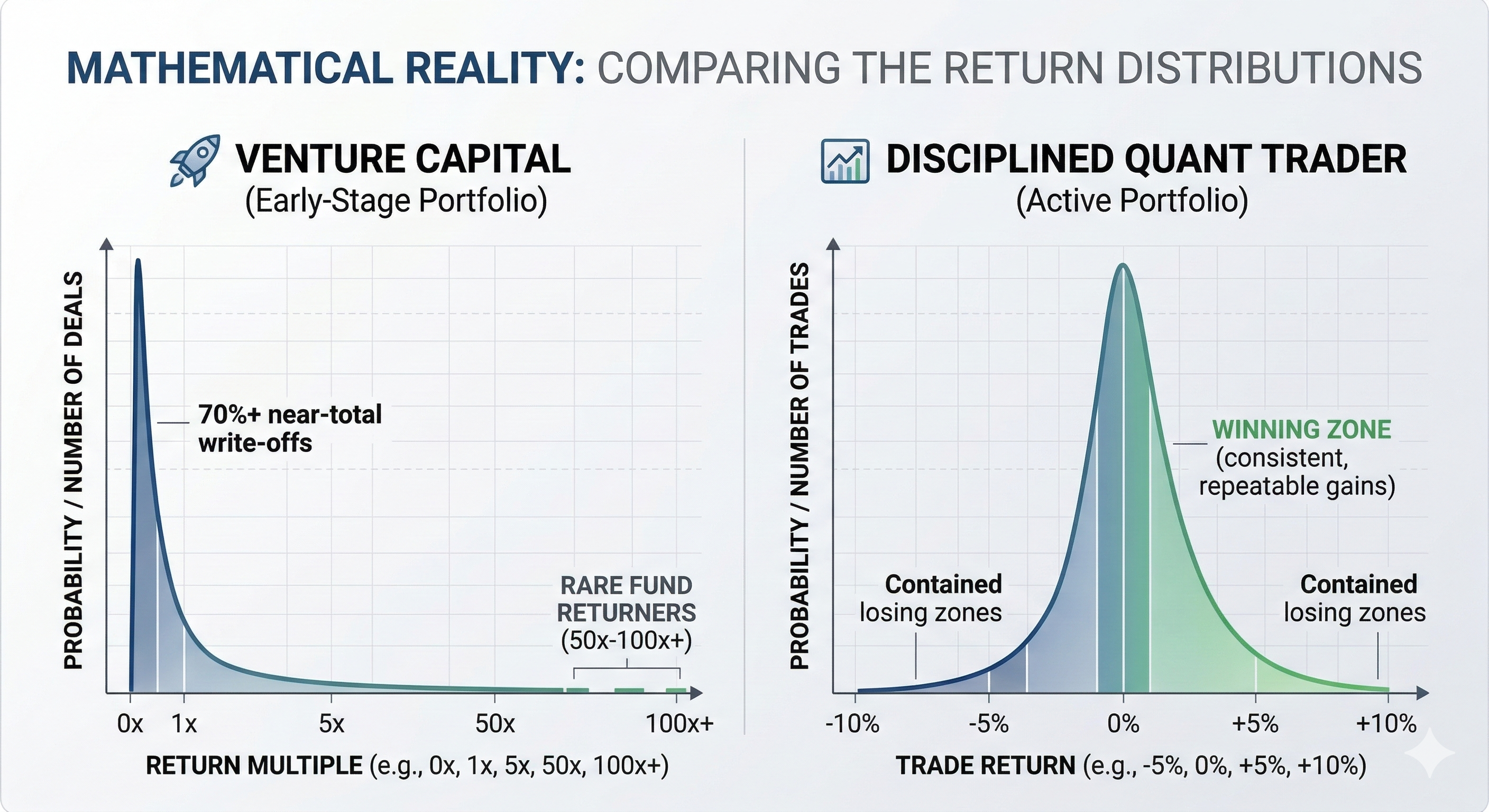

From a probabilistic perspective, VC returns follow an extreme power-law distribution—fat-tailed and Pareto-like, not a normal bell curve. Recent data and benchmarks confirm the structure:

- Win rate: Only about 10–20% of investments return more than 1x invested capital.

- Home run rate: True outliers (10x+ multiples that actually drive fund performance) occur in roughly 1–4% of deals.

- Loss rate: 60–80%+ of deals result in little to no return.

- Return skew: Nearly 80–90% of a fund’s net returns come from the top 1–5% of investments.

The Math of Extreme Variance

This isn’t traditional diversification. It’s deliberate exposure to rare, massive positive tail events. A fund’s portfolio survives only because the asymmetry is extreme: average winners must deliver 30-50x+ multiples (after fees and dilution) just to offset the zeros and produce strong fund-level outcomes.

Mathematically, this is a low-probability, high-reward strategy with brutal expectancy requirements:

Expected Return ≈ (Win Rate × Average Win Multiple) − (Loss Rate × Average Loss Multiple)

Because the win rate is so low and the loss rate is so high, the winning multiple must be massive just to sustain positive expectancy.

The Framing Double Standard: VC vs. Day Trading

Intellectually, early-stage VC isn’t fundamentally different from high-conviction, mathematically driven day trading—it’s the same probabilistic structure with tweaked parameters.

Both systems chase extreme asymmetry: tiny win rates, brutal loss rates, and reliance on rare massive winners. Yet day traders get labeled reckless gamblers, while VC partners are hailed as visionaries.

VC’s slow feedback burn (7-12+ years per deal), the institutional fee wrapper, and a masterful marketing machine let luck masquerade as repeatable genius far more convincingly. The skill narrative was further amplified by the extended zero-interest-rate period (ZIRP), where cheap money created IRRs based on macro tailwinds rather than picking acumen.

The Proof: Simulation Results

To illustrate how extreme this variance is, we ran a Monte Carlo simulation (50,000 iterations). We tested a standard early-stage VC fund against a mathematically disciplined, first-principles trading system (similar to a statistical arbitrage or high-probability options seller).

Here is how the systems compare:

| Business System | Typical Outcome Structure | Target Sample Size (N) | Probability of System Success (>1x) |

|---|---|---|---|

| Venture Capital Fund | Exponential Power Law | N = 30 deals | ~54% |

| Disciplined Math Trader | Normal Distribution (Tight edge) | N = 500+ trades | >99.9% |

(Note: The disciplined trader was modeled with a 56% win rate, 44% loss rate, and a strict 1:1 risk/reward.)

The disciplined system wins mathematically because it maximizes the win rate and the sample size. Even grinding out a modest 56% win rate at a 1:1 risk/reward, the Law of Large Numbers takes over across 500 events, dropping the probability of a losing cycle to near absolute zero.

The VC fund, despite its glamour, is highly dependent on capturing that rare 100x moonshot within a very small 30-deal sample. That is why the probability of a fund merely breaking even is essentially a coin flip.

Caveat: The disciplined system has a much higher probability of success, but a lower ceiling on absolute dollars. True VC outliers have compounded massive absolute wealth by repeatedly nailing the tail over decades. But they are the exception, not the rule.

First Principles Over Hype

For a two-person startup searching for product-market fit, swinging for the fences and embracing power-law dynamics is often a necessary operating system. But for a scaling or mid-market company with a proven model, adopting that same high-variance, hype-driven mindset is a massive liability.

That’s exactly why I founded Unconventional Strategy Partners.

We work with mid-market CEOs, founders, and operators who want to transition away from power-law gambling and scale using rigorous, first-principles thinking. We help you strip away the industry noise and find the actual mathematical levers that drive your business forward.

We focus on:

- AI-leveraged architectures for real, measurable efficiency gains.

- Elite metrics and processes that target >50% win rates in key decisions, rather than 10% moonshots.

- Streamlined operations that turn uncertainty into controlled asymmetry.

If this breakdown resonated with you, and you appreciate an unconventional, mathematically grounded approach to business building, let’s connect.

Send me a message or reach out, and let’s see if we can help you find the highest-probability levers for your operation by stripping away the noise.