The Ugly Truth: The Ergodicity of Ego: Why High-Validity Professionals Fail in Markets

Visualizing the intersection of rigid engineering structures and fluid market data.

Visualizing the intersection of rigid engineering structures and fluid market data.

The Domain-Transfer Paradox

In the deterministic worlds of engineering, science, medicine, and law, certain qualities are golden: persistence, root-cause analysis, and deep domain expertise. These skills deliver reliable, repeatable results because the underlying systems are largely stationary or semi-deterministic. In these fields, intelligence plus effort yields a linear, outsized edge.

Financial markets operate under a completely different set of Kolmogorov axioms. Prices follow processes that are fundamentally probabilistic, characterized by Geometric Brownian Motion (GBM) coupled with a fragile, low-amplitude layer of predictability. This duality tempts the analytically gifted into an “Expertise Trap,” leading to the systematic liquidation of professional capital.

I. The Deterministic Illusion: Why Transfer Learning Fails

In engineering, you solve for X; in markets, X is a moving target that reacts to your observation.

In engineering, you solve for X; in markets, X is a moving target that reacts to your observation.

In engineering or medicine, you can pre-train on massive, structured data and fine-tune to new but similar problems. Domain similarity is high, underlying processes are stationary, and the environment isn’t adversarial.

An engineer mastering control theory transfers it to robotics because the physics do not change. A doctor skilled in differential diagnosis adapts it across specialties because the human body has consistent causal structures. In Machine Learning terms, Transfer Learning works wonders in these domains. In markets, it is your worst enemy.

Markets flip every assumption:

- Extreme Non-Stationarity: Regimes shift constantly (volatility clusters, policy shocks). What predicted returns in one decade poisons the next.

- Adversarial Self-Correction: Profitable patterns get arbitraged away as capital flows in.

- Low Signal-to-Noise Ratio (SNR): Predictable components are weak and buried in massive diffusive noise.

II. The Physics of Failure: Drift vs. Diffusion

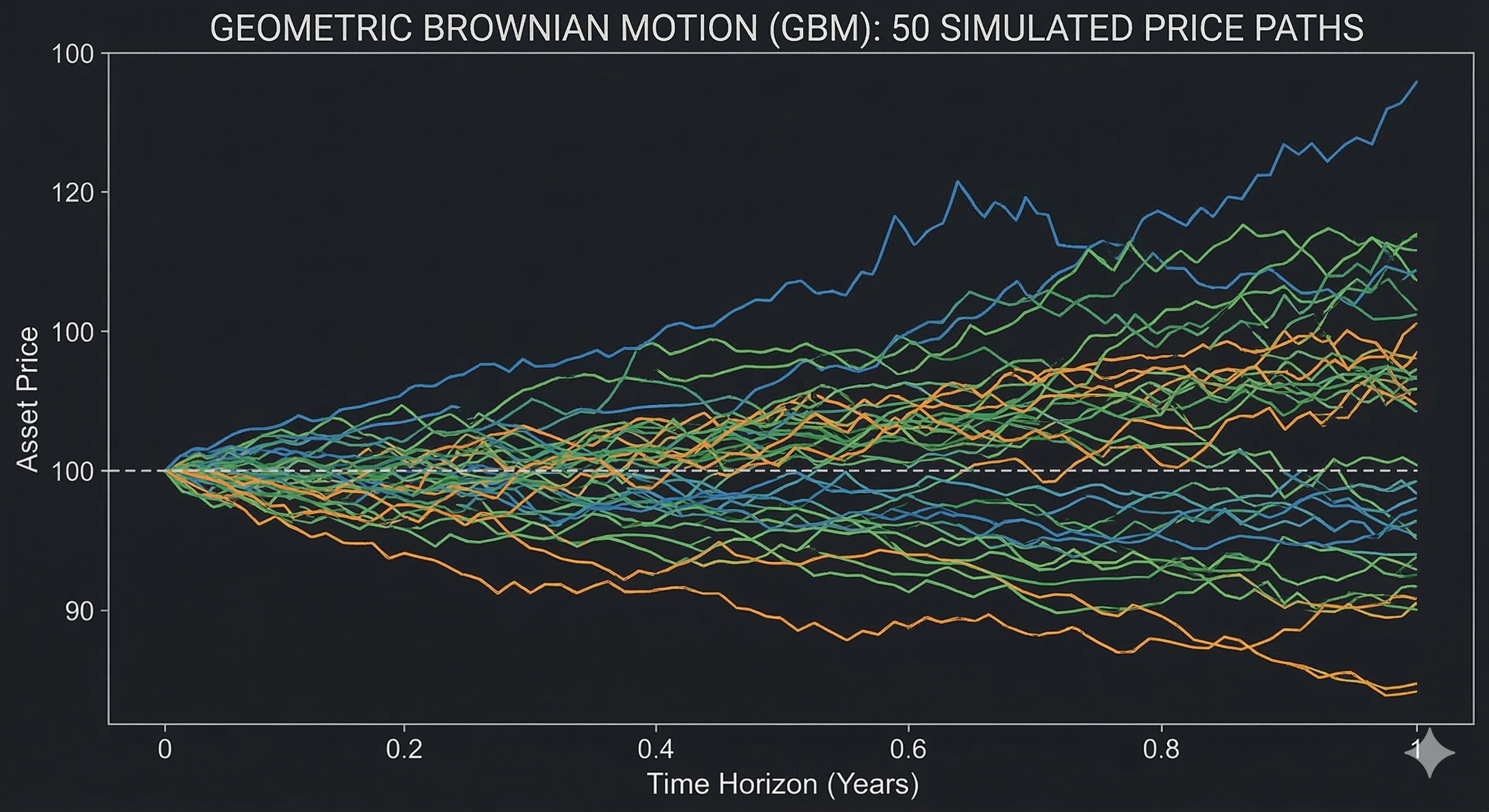

In engineering, we are trained to minimize “noise” to reveal “signal.” In markets, the noise is the signal. To formalize this, we must look at the stochastic process at the heart of market dynamics. Price paths closely resemble Geometric Brownian Motion (GBM), defined by the Stochastic Differential Equation (SDE):

$$dS_t = \mu S_t , dt + \sigma S_t , dW_t$$

Where \(W_t\) is a Wiener process (standard Brownian motion), \(\mu\) is drift, and \(\sigma\) is volatility. To visualize why “persistence” fails the professional, we look at the discrete simulation:

$$S_{t+1} = S_t \exp\left( \left(\mu - \frac{\sigma^2}{2}\right)\Delta t + \sigma \sqrt{\Delta t} , Z \right), \quad Z \sim \mathcal{N}(0,1)$$

Simulated price paths showing how variance (noise) dominates drift (signal) over short horizons.

Simulated price paths showing how variance (noise) dominates drift (signal) over short horizons.

These paths are diffusive: variance grows linearly with time, and long-term behavior looks like a random walk with mild drift. The “Professional’s Hubris” is a failure to respect the Estimation Risk of the drift \(\mu\). Mathematically, the variance of the drift estimator \(\hat{\mu}\) over a time horizon \(T\) is:

$$\text{Var}(\hat{\mu}) = \frac{\sigma^2}{T}$$

The error in estimating your “edge” does not depend on the frequency of your data (the engineer’s obsession with “more data points”), but strictly on the total time elapsed \(T\). To estimate a \(10\%\) return with \(20\%\) volatility to within a \(1\%\) error margin, you mathematically require 400 years of data.

III. Fragile Predictability and the ML Pivot

Despite the Brownian dominance, there is “some amount of predictability.” Recent microstructure research (e.g., 2025 arXiv papers) explains why prices remain Brownian-like despite predictable institutional order flow: the square-root law of impact enforces diffusion, mitigating large moves and preserving efficient-market behavior.

Predictability exists in:

- Short-term momentum/mean-reversion.

- Volatility clustering (GARCH effects).

- Order-flow persistence from metaorders (Lillo-Mike-Farmer models).

The ML Trap: Feature Over-Engineering

High-IQ professionals often suffer from feature over-engineering. They look at macro-economics or news—features that are lagged or “priced in.” ML models can detect weak signals in backtests (Sharpe > 1 in-sample), but live performance decays fast due to non-stationarity.

![]() Reducing the feature space to raw price movement to avoid overfitting narrative noise.

Reducing the feature space to raw price movement to avoid overfitting narrative noise.

The retailtrader.ai approach corrects this by focusing purely on Price Action (PA). By reducing the feature space to the rawest form of market intent, we perform a form of Dimensionality Reduction, stripping away the “narrative noise” that causes engineers to overfit.

IV. The Behavioral Breakdown: Why Scientists, Doctors and Lawyers Lose

Behavioral finance (Barber & Odean) confirms that high-achieving professionals systematically underperform. This is rooted in three formal errors:

- The Illusion of Control: Professionals are “fixers.” In markets, doubling down on a losing trade violates the Kelly Criterion \( (f^* = \frac{\mu}{\sigma^2}) \), which demands we shrink position sizes as volatility rises.

- Narrative Overfitting: Lawyers are trained to build “cases.” In markets, this leads to fitting a logical story to a random walk—post-hoc narrative chasing.

- The Disposition Effect: Professionals equate being “wrong” with failure. They hold losers to avoid bruising their ego, whereas markets require Bayesian Updating: the moment the Price Action invalidates the prior, the position must be terminated.

Precision tools (multiple monitors, fast data) are useless if the underlying mindset is deterministic.

Precision tools (multiple monitors, fast data) are useless if the underlying mindset is deterministic.

V. The Winning Mindset: Adapt or Perish

To survive, the professional must pivot from “Solving the Market” to “Trading the Probabilities.”

- Discard Transfer Learning: Treat markets as a new, adversarial domain.

- Price Action over Narrative: Focus on the “Tape” where probability is in your favor. Don’t predict the “bird’s” final destination; predict the next 10 feet based on momentum.

- Risk as the “Root Cause”: In engineering, failure is a bug. In trading, failure (a losing trade) is a statistical cost of doing business. Apply persistence to your discipline, not your positions.

- Meta-Learning: Focus on surviving regime shifts. Use your skills for process, not just prediction: Monte Carlo risk sims, walk-forward testing, and volatility targeting.

Summary: The Cognitive Pivot

| Feature | Engineering/Medical Mindset (Failure) | PA-Probabilistic Mindset (Survival) |

|---|---|---|

| Data Source | External “Root Causes” (News/Macro) | Pure Price Action (The Tape) |

| Logic Type | Deductive: “If A, then B.” | Probabilistic: “PA shows 60% chance of X.” |

| Persistence | Holding the line until it works. | Ruthless liquidation when PA shifts. |

| Goal | To be “Right” (Zero Error). | To be “Profitable” (Positive Expectancy). |

Conclusion

Markets are not purely random, nor are they solvable equations. They are Brownian motion coupled with fragile, PA-driven predictability—enough to lure the analytically elite, yet structured to punish those who refuse to adapt. The qualities that make you exceptional at your day job will be your undoing here. Throw deterministic thinking out. Play the probabilistic game: manage risk obsessively, trade the Price Action where you have an edge, and let time plus discipline do the heavy lifting.