The Ugly Truth: The $730 Billion Elephant in the Room: Why SoftBank Could Be the Pin That Pricks the AI Bubble

As a retail trader, my bread and butter is the short-term: momentum, technical breakouts, and rapid execution. But surviving in the markets requires periodically stepping out of the trenches. It requires adopting a contrarian, long-term philosophy—akin to the legendary Ken Fisher—that forces you to question the prevailing noise, look at market history, and spot the macro risks that everyone else is too euphoric to see.

Right now, the market is blindingly euphoric about Artificial Intelligence. But if you zoom out and look closely at the financial engineering funding this boom, you’ll spot a massive elephant stomping around the room: SoftBank Group (SFTBY).

While the broader financial media remains transfixed by the sheer size of the numbers being thrown around, a closer look at SoftBank’s balance sheet reveals a high-stakes drama. It begs a critical question: Is SoftBank’s recent pivot to AI a masterclass in visionary investing, or is it the exact pin that will prick the bubble?

(Note: Use the 4-panel visual generated earlier here to hook the reader’s attention)

(Note: Use the 4-panel visual generated earlier here to hook the reader’s attention)

The Illusion of Triumphant Earnings

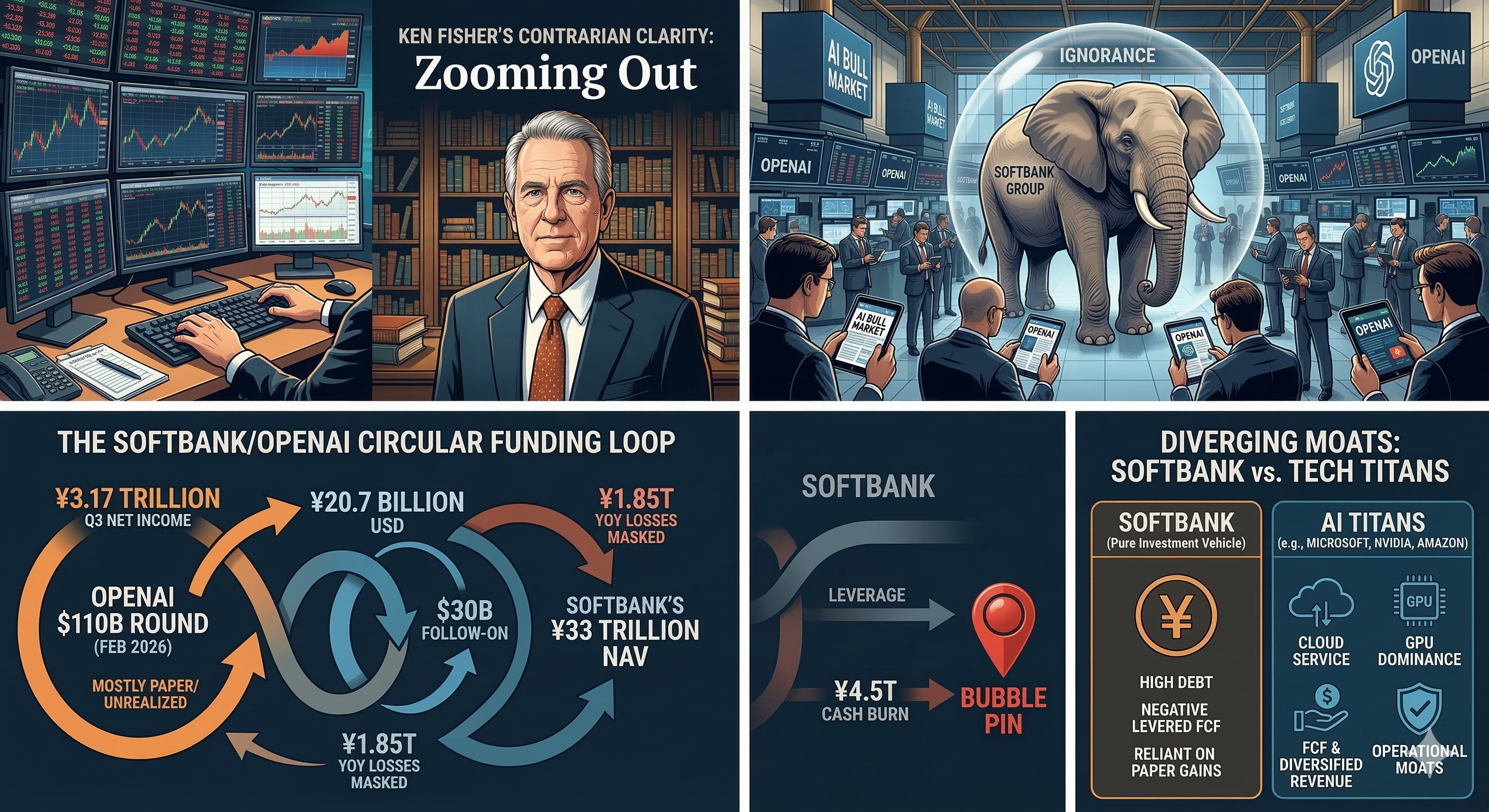

On the surface, SoftBank’s Q3 FY2025 earnings (released February 12, 2026) looked like a total vindication of Masayoshi Son’s aggressive AI pivot. The company reported a staggering net income attributable to owners of ¥3.17 trillion (about $20.7 billion USD)—a massive ¥2.54 trillion year-over-year jump. This marked their fourth consecutive quarterly profit. Return on Equity (ROE) hovered around an enviable 23-24%, with net margins nearing 49%. NAV recovered to roughly ¥33 trillion pro forma.

It looked triumphant. But to a trader, the anatomy of this profit jump looks suspiciously like a classic portfolio-masking maneuver: closing out your green positions to create the illusion of profitability while holding onto heavy bags.

SoftBank’s ¥3.17 trillion profit was heavily driven by the sale of its entire stake in Nvidia last October for roughly $5.8 billion, delivering ¥339.1 billion in realized gains. It was a brilliant trade, but without it, SoftBank’s holding companies segment would have swung sharply negative, dragged down by a ¥1.85 trillion YoY drop featuring massive losses in legacy bets like T-Mobile (¥-630 billion) and Alibaba (¥-168 billion).

The real mask hiding SoftBank’s core vulnerabilities is its exposure to OpenAI. By the end of December 2025, SoftBank had recorded an investment gain on OpenAI of about $19.8 billion. However, the vast majority of this “profit” is a mirage of unrealized, paper gains.

The OpenAI Feedback Loop

The financial interdependence between SoftBank and the AI ecosystem is getting wild. In late February 2026, OpenAI announced a historic $110 billion funding round at a staggering $730 billion pre-money valuation (pushing post-money to roughly $840 billion). SoftBank contributed a whopping $30 billion to this round, pushing its cumulative investment in OpenAI to $64.6 billion and securing roughly a 13% ownership stake.

SoftBank is essentially funding the very valuation rounds that are propping up its own Net Asset Value (NAV). They are paying OpenAI $3 billion annually for Japan rights, while concurrently funneling hundreds of millions to other portfolio companies like Arm to maintain the ecosystem. It is a circular loop of capital that props up the balance sheet but exposes SoftBank to catastrophic volatility if the music ever stops.

Leverage, Debt, and the Cracks in the Foundation

The financial cracks are already showing for those willing to look past the AI hype:

- Credit Downgrades: On March 3, 2026, S&P lowered SoftBank’s outlook to negative, citing the danger that its massive, concentrated OpenAI bets are eroding the credit quality of its assets and hurting liquidity. Jefferies similarly downgraded them to Underperform over leverage concerns.

- The Debt Hunt: To fund this $30 billion commitment, SoftBank is reportedly seeking a record-breaking $40 billion bridge loan. Based on early March reports, these are ongoing discussions, meaning SoftBank is actively trying to underwrite massive new debt in a tightening environment just to maintain its seat at the AI table.

- Deteriorating Metrics: Cash burn has accelerated, with investing outflows hitting ¥-4.5 trillion in the nine months leading up to Q3. SG&A ballooned by ¥359 billion, and finance costs rose by ¥110 billion. Liquidity ratios have dipped below 1 (current/quick ~0.83/0.81), and debt-to-equity is hovering uncomfortably near 0.96–1.32.

Diverging Moats: SoftBank vs. The Tech Titans

It’s true that SoftBank isn’t the only giant pouring billions into OpenAI. The February 2026 mega-round also included $50 billion from Amazon and $30 billion from Nvidia. Microsoft and AMD are also deeply entangled in the AI infrastructure race.

But there is a fundamental difference between SoftBank and the American tech titans: Operational Moats.

- Microsoft ($3T+ Market Cap): MSFT has diversified moats. Their exposure is turned into immediate operating profit via Azure (seeing 28%+ YoY growth on AI workloads), Office copilots, and GitHub. They boast 39% margins and massive free cash flow.

- Amazon: AMZN’s $50 billion OpenAI commitment is heavily tied to AWS exclusivity and massive compute agreements. It’s not just cash out the door; it’s a revenue-generating partnership that feeds directly into their core cloud infrastructure business.

- Nvidia & AMD: NVDA and AMD are supplying the literal picks and shovels. Their investments are largely supply-deal oriented (e.g., AMD’s multi-year GPU supply deal for 6GW compute).

If AI valuations experience a cooldown, Microsoft, Amazon, Nvidia, and AMD have massive, diversified, cash-flowing businesses to fall back on. SoftBank does not. As a pure investment vehicle with negative levered free cash flow and mounting debt, SoftBank’s $64.6 billion OpenAI bet lacks an operational backstop. They are a pure, levered equity play.

The Price Action Tells the True Story

The market is starting to sniff this out, even if the financial media isn’t talking about it.

Despite the $110 billion OpenAI hype, SoftBank’s stock (SFTBY) closed at $12.04 on March 11, 2026, and has traded as low as ~$11.05–$11.90 in recent intraday sessions (March 12). It remains down roughly 15-17% YTD from its $14.36 start to the year, and miles below its 52-week high of $22.50. It is trading well below both its 50-day and 200-day moving averages.

While the broader Nikkei is up ~8% and peers remain resilient, SFTBY is lagging noticeably. Furthermore, there is a massive discrepancy between SoftBank’s claimed ¥33 trillion pro forma NAV and its actual market capitalization.

The stock price is reflecting what the headlines are ignoring: the sheer weight of leverage and concentrated bet risk. The market simply does not believe SoftBank’s internal math or the liquidity of those paper gains.

The Eerie Silence

Perhaps the most concerning part of this entire setup is the news vacuum. Following the initial buzz of the Q3 earnings and the February $110 billion OpenAI round, there has been an eerie silence. X (formerly Twitter) chatter regarding SoftBank’s leverage is thin. There are no viral threads warning about the illusionary profits or the S&P downgrade.

The AI euphoria is so loud that it is drowning out basic risk management. But as contrarian investors know, the biggest risks aren’t the ones everyone is screaming about—they are the ones hiding in plain sight. SoftBank has positioned itself as the undisputed whale of the AI boom. But if the valuations stall, or if the debt becomes too expensive to service, this elephant won’t just stumble. It could bring the whole circus down with it.